When the U.S. Federal Reserve cut the rate to zero, investors that depended on safe, fixed income instruments suffered. The sharply lower bond yields and lack of return from cash forced retirees to invest in the stock market. And because most sectors rose sharply in the last year, dividend-income investors must contend with falling yields and a higher stock price. Despite needing to pay more after stocks went up, investors may look for dividend stocks to buy.

Retirees may look at dividends as a measure of the health of a company, but should not look at the yield alone. Hayong Yun, associate professor of finance at Broad College of Business at Michigan State University, says to equate a company’s health to the excess cash it generates. “When companies are doing well with high sales, their revenue will exceed expenses and are left with excess cash, which can be returned to shareholders as dividends,” said Prof. Yun.

Companies like Apple (NASDAQ:AAPL), if it is at a mature phase, pay a low dividend yield. The company is choosing to re-invest its excess cash to pursue growth opportunities.

There are seven dividend stocks to buy for retirees that consider the company’s business health against its dividend yield. The companies are:

- AbbVie Inc. (NYSE:ABBV)

- Altria Group (NYSE:MO)

- AT&T (NYSE:T)

- Takeda Pharmaceutical (NYSE:TAK)

- 3M Company (NYSE:MMM)

- CVS Health (NYSE:CVS)

- ONEOK (NYSE:OKE)

AbbVie Inc. (ABBV)

Source: Piotr Swat / Shutterstock.com

First up on this list of dividend stocks to buy is AbbVie. Drug manufacturer AbbVie spent its excess cash on hand and raised debt to buy undervalued drug companies. It most recently bought Allergan to bolster its aesthetics unit. The timing proved unlucky and hurt short-term results. Allergan’s Botox Therapeutics fell during the Covid-19 disruption earlier this year.

CEO Rick Gonzalez said that the business rebounded strongly in the second quarter. It is now tracking close to 95% to 100% of previous pre-Covid levels. Allergan has no real competition since its peers are smaller. So, as a market leader in the aesthetics business, it may expand margins by building on its strong direct-to-consumer channels.

The company plans to invest more than when Allergan was on its own. It wants to drive patients from the DTC and digital channels in the coming quarters. This will increase the return from the takeover.

Assuming a modest discount rate of 7% and revenue growing in the single digit, dividend stocks to buy like AbbVie stock is worth at least $100:

| Metrics | Range | Conclusion |

| Discount Rate | 7.5% – 6.5% | 7% |

| Perpetuity Growth Rate | 3.5% – 4.5% | 4% |

| Fair Value | $65.04 – $171.72 | $100.61 |

ABBV stock pays a $4.72 annual dividend. Its debt/equity is almost 6 times, which may scare off cautious investors. So long as Allergan’s cash flow grows, AbbVie may achieve both a debt reduction and a growing dividend.

Altria Group (MO)

Source: Kristi Blokhin / Shutterstock.com

Tobacco firm Altria is a consumer defensive company whose days of expensive acquisitions are at an end. The company invested in Cronos (NASDAQ:CRON) only to see the cannabis valuations shrink considerably. Its Juul investment led to a $4.5 billion write-down last year.

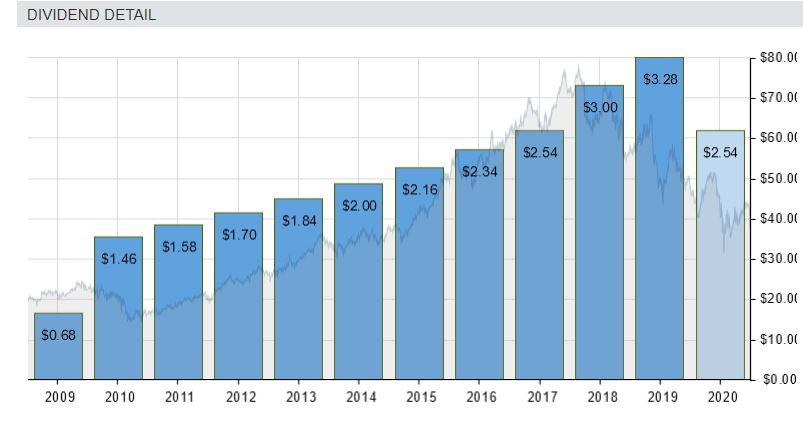

If expensive acquisitions ended, then Altria may build its cash position in the quarters ahead. It may even increase its $3.44 annual dividend, which yields close to 9%. If it buys back shares, its price-to-earnings will decline. The tobacco firm is not a risk-free trade. Covid-19 is dangerous to those with pre-existing health conditions, including unhealthy lungs.

As shown above, Altria consistently raised dividends in the last decade. This year, dividends will top $3.44 a share.

If there is a negative association between long-time smokers and higher mortality from Covid-19, that would hurt MO stock. And if Juul’s e-vaping product decreases a person’s immunity in fighting Covid-19, Juul’s value to Altria will fall. The market’s opinion on Altria will cycle between caution and a positive willingness to buy shares for the dividend. As fear mounts and Altria shares fall, retirees may consider buying the stock at discounted prices.

AT&T (T)

Source: Jonathan Weiss/Shutterstock

The repeated commitments from AT&T’s CEO to increase its payout ratio to sustain the dividend is preventing the stock from falling further. At a dividend yield that cycles between the 6% and 7% range, income investors should look at this telecom services firm.

AT&T’s ill-timed WarnerMedia buyout raised its debt to unhealthy levels. The firm’s strategy in paying down debt depended on steady subscription fees from mobile and cable customers. Closed movie theatres and a slowdown in film and television production are hurting WarnerMedia studios’ business. The negative cash burn needs to end.

Until the Covid-19 pandemic ends, AT&T has no idea when the studio will recover. The increasing levels of uncertainties are weighing on T stock, while creating another entry point for retirees looking for an inexpensive investment that pays a high dividend yield.

On Tipranks, the average one-year price target is $33.40.

Takeda Pharmaceutical (TAK)

Source: Jonathan Weiss / Shutterstock.com

After acquiring Shire Pharmaceuticals in 2019, Takeda continues to shed assets to raise cash and pay down debt. The deal cost $62.2 billion, but with Shire’s debt included, the total cost was closer to $80 billion.

On Sept. 16, the firm sold TachoSil to Corza Health for EUR 350 million. TachoSil is a surgical patch that assists in bleeding control. Takeda reported yearly revenue of $160 million from the product. The expansion of a new research and development cell therapy manufacturing facility suggests that the company is not cutting down on its investments.

In its first quarter, Takeda posted revenue growing 0.9% year on year. 83% of its revenue is from five key business areas. As a mature firm, TAK stock yields around 4.5%. Unlikely to change in the near-term, the debt reduction and continued R&D investments may reward long-term investors. A dividend hike may eventually come as Takeda launches new products to market.

3M Company (MMM)

Source: JPstock / Shutterstock.com

After rising steadily throughout the last year, 3M’s stock continues to reward existing shareholders. Still, income investors will get a dividend in the 3.5% range. Known best for its Personal Protective Equipment (PPE), the continued sales growth assures the dividend payout rate will not change.

On Sept. 15, 3M posted August sales of $2.7 billion, up 2% Y/Y. In Health Care, sales grew 23%. Safety and Industry enjoyed a 6% Y/Y growth while the Consumer unit grew 3%. Only Transportation and Electronics lagged, falling 11% from last year. MMM stock should enjoy its uptrend after forecasting third-quarter revenue in the range of $8.2 billion to $8.3 billion.

3M will post its Q3 results on Oct. 27.

Increasing demand for PPP as Covid-19 infections increase in the weeks ahead may lift 3M’s revenue forecast for the next quarter. That is just another reason to own 3M stock. On Wall Street, the average price target is around $167 (per Tipranks).

CVS Health (CVS)

Source: Jonathan Weiss / Shutterstock.com

In the pharmaceutical retail space, bearishness is mounting ahead of the U.S. elections. Uncertainties in what Medicare will look like are hurting CVS Health stock. Last week, the stock bounced back from the ~$57 level as investors speculated on a rebound.

CVS reaffirmed its full-year adjusted EPS guidance. It expects an adjusted EPS in the range of $7.14 – $7.27. GAAP EPS guidance is lower than the previous figures as the company pays back debt earlier. Cash flow from operations will be $11 billion to $11.5 billion.

CVS has long-term debt and capital lease obligations of $82 billion. Its acquisition of Aetna hurt its balance sheet but strengthens its business. The retired investors will notice the strong operating cash yield will easily cover the dividend.

Instead of holding cash that pays below 0.1% interest, dividends from CVS are more attractive. This 5-year discounted cash flow model suggests that CVS stock is worth at least $85 (the link opens editable, interactive finbox model).

ONEOK (OKE)

Source: Shutterstock

The final stock on this list of dividend stocks to buy is Oneok. In the oil and gas midstream sector, Oneok is a compelling stock to consider. Investors should exercise caution on this stock due to the weakness in the sector. In the second quarter, Oneok posted a net income of $134.3 million. Adjusted EBITDA was $533.9 million. It ended the quarter with over $945 million in cash and cash equivalents.

OKE stock is down around 60% from yearly highs. The stock moved nowhere since July as markets adopted a wait and see approach. In its investor presentation, the company reported that it has well-capitalized customers. No single customer accounted for more than Oneok’s revenue. It cut $900 million from its capital spending by pausing several projects.

The company will declare dividends around Oct. 23. If it is in-line with the previous payment, investors who exited the stock may come back in. More importantly, if natural gas prices improve, then so too will Oneok’s revenue prospects.

Related: You NEED to See This Photo…

Take a look at this photo, shot by the Mayo Clinic’s most elite researchers:

These two elderly mice are exactly the same age.

But as you can see…

The one on the left is graying and frail, as you’d expect an elderly mouse to be…

And the mouse on the right is strong, healthy, and showing none of the symptoms of aging.

How can this be possible?

The answer is simple:

Because of the groundbreaking new technology contained within this pill…

Which is undergoing human trials as we speak.

As you will see in this special presentation…

We’re about to witness the biggest medical breakthrough in history…

In fact, I believe that investors who set themselves up to profit from it could turn every $500 invested into as much as $1.5 million.