For investors remaining sidelined after the market’s impressive bounce back, the opportunity may now be too enticing to ignore. According to J.P. Morgan strategist Nikolaos Panigirtzoglou, COVID-19 will drive equity supply growth as companies pivot away from buybacks in an effort to raise capital, with 2019 marking the first time since 2015 that the net supply of shares, or the share issuance adjusted for de-listings and buybacks, increased materially.

Alarming for investors, the previous decade-long trend of declining equity supply in part fueled the market’s bull run as buybacks pushed earnings higher. Some analysts also point out that a larger equity supply could weigh on stocks and cause volatility if companies don’t purchase shares when their stocks fall.

Panigirtzoglou, however, takes a different stance. He notes that the drop in buybacks hasn’t negatively impacted the market yet. In fact, he argues the low returns for both bonds and cash will ultimately create an environment that makes equities attractive.

“Our most holistic of our equity position metrics, which compares the size of the equity universe to the size of the bond and cash universe, implies 47% upside for equities from here assuming the implied equity allocation of non-bank investors globally rises from 40% currently to the post Lehman period high of 49%,” Panigirtzoglou commented.

Taking all of this into consideration, we ran three J.P. Morgan-approved stocks, which each boast over 40% upside potential according to the firm’s analysts, through TipRanks’ database to get the rest of the Street’s opinion.

Editor's Note: Millennial Discovers Weird Market Hack. Everyday Americans Thrilled

Taylor Morrison (TMHC)

Taking its place as one of the largest home building companies in the U.S., Taylor Morrison uses its resources, support and industry experience to make the development process easier for its clients. While shares took a nasty tumble earlier this year, J.P. Morgan believes that any weakness presents a buying opportunity.

Representing the firm, analyst Michael Rehaut is now taking a more bullish approach when it comes to this name. Pointing to its valuation, he sees the “highly discounted valuation relative to its peers as attractive against our fundamental outlook for the company.”

Expounding on this, Rehaut stated, “Specifically, TMHC trades at 8.2x and 6.4x our 2020E and 2021E EPS, respectively, significantly below its smaller-cap peers’ averages of 10.0x and 9.5x, while additionally, we point to the stock’s P/B of 0.9x, well below its peers’ 1.3x average. We view this relative valuation as not properly reflecting our fundamental outlook for the company, which features 2021E operating margins of 8.1%, roughly in-line with its smaller cap peers’ average, as well as our 2021E ROE of 11.6%, which we note is only modestly below its peers’ 12.2% average.”

To support his optimistic stance, Rehaut cites the demand improvement over the last two months, “which has resulted in a likewise improvement in earnings visibility.” He added, “We believe, on average, current P/E multiples are appropriate relative to the current backdrop, as we note that these levels are close to the group’s longer-term mid-cycle average valuation, which we view as reasonable given that housing starts were approaching their long-term averages prior to the current COVID-19 pandemic, towards which we believe demand is currently reverting.”

To this end, Rehaut rates TMHC an Overweight (i.e. Buy) along with a $27 price target. This new target puts the upside potential at 42%.

Judging by the consensus breakdown, 4 Buys and 2 Holds received in the last three months merge to a Moderate Buy rating from the analyst consensus. Given the $20.67 average price target, the upside potential lands at 9%.

Editor's Note: Your shot to collect $1,000 to $5,000 a week – regardless of how volatile the markets are swinging.

Michaels Companies (MIK)

Known for being the largest arts and crafts retail chain in North America, Michaels Companies also owns several brands that enable it to offer arts, crafts, framing, floral, home décor and seasonal merchandise to decorators. Even though year-to-date, shares are in the red, MIK has staged an impressive recovery in the last three months, adding a whopping 339% to its share price.

Writing for J.P. Morgan, 5-star analyst Christopher Horvers tells clients that optimism regarding the pace of economic recovery and a wide divide in valuation for essential retailers and value-levered companies prompted him to scan his coverage universe for upgrade opportunities.

Enter MIK. Horvers believes that this stock reflects “the best upside potential at current prices.” As a result, MIK scores a spot on J.P. Morgan’s U.S. Equity Analyst Focus List as a value idea “based on an expected re-rating to PE on 2021 EPS due to the path to positive comps over the next four quarters, new management, and improving margin performance into 2021.”

Looking at its valuation, MIK trades at 3x P/E using Horvers’ 2021 forecast, equivalent to 4.8x EV/EBITDA, because investors remain fixated on its low growth rate, -LSD comp rate since 4Q18 and its leverage, which were all negative factors in 2020.

Horvers explained, “MIK is inexpensive relative to history… While valuation has collapsed since comps turned negative in 2018 (averaging 6.0x PE since), it traded at an average of 13x in the 2014-17 period when comps were better. This is in comparison to quality/’growth’ retail stocks (and the market), which have broadly been trading in-line to above recent historical averages (HD at 23x P/E on 2021E vs. FY1 average of 21x, WMT at 22x vs. 21x, and COST at 33x vs. 31x).”

Speaking to the AC Moore opportunity and management’s digital efforts, Horvers sees positive comps on the horizon in the near-term. He noted, “Moreover, as discussed below, we believe new CEO Ashley Buchanan (former WMT US eCommerce EVP) can turn the tide of share losses. Then, we get the lapping of closed stores in 1H21.” The analyst also thinks MIK’s leading position in an enthusiast-based category as well as investments in e-commerce, price perception and innovation should help reverse share loss. If that wasn’t enough, 2020 could see pressure on margins diminish, with strong expansion slated for 2021.

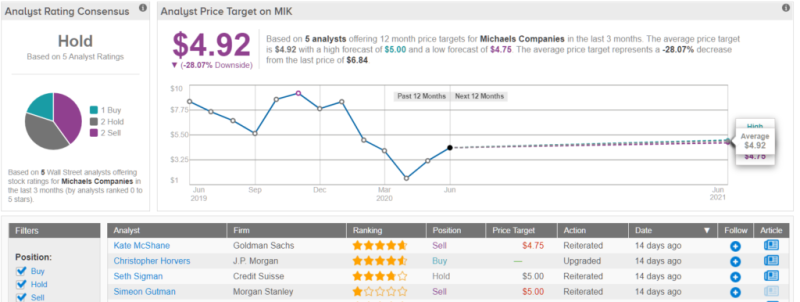

In line with his bullish take, Horvers gave the rating a boost, upgrading MIK from Neutral to Overweight. The price target also gets a $6 lift, with it now landing at $13. This target conveys his confidence in MIK’s ability to soar 90% in the next year.

As for the broader analyst community, other pros are more cautious. 1 Buy, 2 Holds and 2 Sells add up to a Hold consensus rating. At $4.92, the average price target brings the downside potential to 28%.

Editor's Note: Down and Out Millennial Shares the Strategy that Grew his Money to $5 million in 2 years

As for Banco de Chile, it operates as a bank and financial services company, serving its client base that includes large corporations, SMEs as well as private clients. Given the nature of the company’s clientele, J.P. Morgan is giving the stock a thumbs up.

Analyst Domingos Falavina tells investors that in Chile specifically, COVID-19's economic impact has been much lower than in other countries. That said, he cites several factors that could put BCH even farther ahead of its competitors. Calling it the “place to be in the short term”, the analyst said, “We see Banco de Chile as better prepared to face the potential worsening credit cycle ahead and although some investors can argue its 2.1x P/BV is ‘rich’, we see this premium as deserved.”

To back this up, Falavina points out that BCH serves individuals with a higher net-worth, which bodes well for the company as this group typically sees less of a reduction in credit quality. On top of this, it also has lower exposure to the retail, services, transportation and credit card segments, which tend to be riskier.

Additionally, the banking name boasts the highest level of coverage when compared to other large Chilean banks, with the figure coming in at 209% as of April 2020, factoring in its Chilean peso 238 billion in additional reserves. “Though it dropped from past 250-270% levels in 2017-2018 it still is still higher than Santander Chile at 150%, BCI at 156% and industry at 146%,” Falavina commented.

The good news doesn’t end there. Falavina believes that higher spreads in guaranteed lines and its liability-sensitive nature will make its margins more resilient. Further separating BCH from the crowd, Santander Chile’s Latam loyalty plan may be less appealing for clients and its fee income should be superior to Credicorp’s, according to the J.P. Morgan analyst.

With BCH’s historical premium conveying its higher ROA and coverage, the deal is sealed for Falavina. As a result, he upgraded the stock’s rating to Overweight. Should the $26 price target be met, a twelve-month gain of 41% could be in store.

Turning now to the rest of the Street, it has been quiet when it comes to other analyst activity. Falavina’s rating was the only one issued recently, so the consensus rating is a Moderate Buy.

Related: You Could Make Your Portfolio “Recession-Proof” with This System

While most investors watched their hard-earned money evaporate during the 2008 recession, I collected thousands per week by developing the ultimate indicator. I used it to identify the moves all the big players were quietly making… putting me in the know weeks before others caught on. Today, I’m spilling the beans so that you too can turn any market condition into profits! Click here now.